$18,000

401k and Retirement Plan Limits for the Tax Year 2016

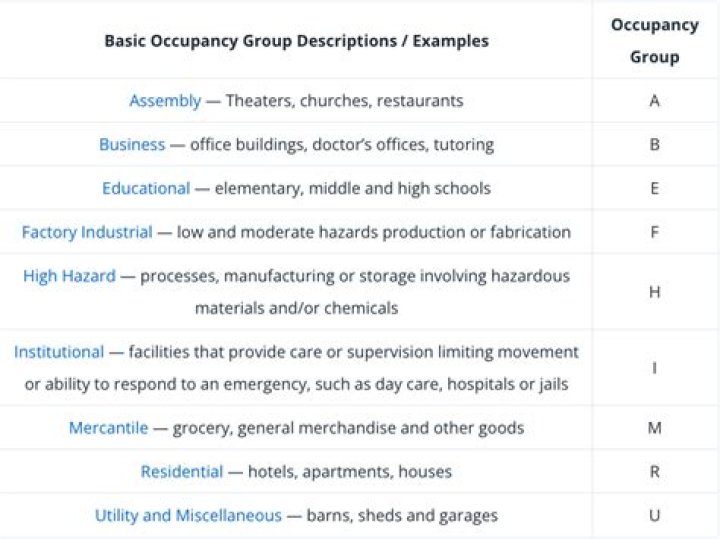

| Chart of Select Limits | ||

|---|---|---|

| 401k Elective Deferrals | $18,000 | $18,000 |

| Annual Defined Contribution Limit | $53,000 | $53,000 |

| Annual Compensation Limit | $265,000 | $265,000 |

| Catch-Up Contribution Limit | $6,000 | $6,000 |

Are 401k deductions tax-deductible?

The contributions you make to your 401(k) plan can reduce your tax liability at the end of the year as well as your tax withholding each pay period. However, you don’t actually take a tax deduction on your income tax return for your 401(k) plan contributions.

How much does 401k contribution save on taxes?

But, with a tax-deferred 401(k), you save taxes on the earnings of your contributions. For example, if you contribute $100 a month into a traditional 401(k) that earns 8%, you could amass more than $150,000 of tax-free retirement savings over 30 years and save almost $50,000 in taxes as your earnings compounded.

Are individual 401k contributions tax-deductible?

In a Solo 401(k) plan all contributions you make as the “employer” will be tax-deductible (subject to IRS maximums) to your business with any earnings growing tax-deferred until withdrawn. Or you can make some or all of your employee deferral contributions as a Roth Solo 401(k) plan contribution.

What is the catch-up contribution for 2016?

$6,000

The catch-up contribution will remain the same, too – you can contribute an extra $6,000 if you’ll be 50 or older anytime in 2016. IRA maximum contributions aren’t changing, either. You will be able to contribute up to $5,500 to an IRA in 2016, plus an extra $1,000 if you’re 50 or older.

What is the catch-up rate for 2016?

1, 2016: 401(k), 403(b) and profit-sharing plan elective deferrals stays at $18,000. The catch-up contribution limit for participants age 50 or older stays at $6,000. (The catch-up limit applies from the start of the year to those turning 50 at any time during the year.)

How do I deduct 401k on my taxes?

Generally, yes, you can deduct 401(k) contributions. Per IRS guidelines, your employer doesn’t include your pre-tax contributions in your taxable income because your 401(k) contributions are tax-deductible. Instead, they report your contributions in boxes 1 and 12, respectively, of your form W-2.

Are you taxed on 401k contributions?

Contributions to qualified retirement plans such as traditional 401(k) plans are made on a pre-tax basis, which removes them from your taxable income and thus reduces the taxes you’ll pay for the year.

Do I need to report my 401k on taxes?

401k contributions are made pre-tax. As such, they are not included in your taxable income. However, if a person takes distributions from their 401k, then by law that income has to be reported on their tax return in order to ensure that the correct amount of taxes will be paid.

Is it better to contribute to 401k before tax or after tax?

Pre-tax contributions may help reduce income taxes in your pre-retirement years while after-tax contributions may help reduce your income tax burden during retirement. You may also save for retirement outside of a retirement plan, such as in an investment account.

Is 401k match taxable?

* Plus, your contributions, any match your employer provides and any earnings in the account (including interest, dividends and capital gains) are all tax-deferred. That means you don’t owe any income tax until you withdraw from your account, typically after you retire.

Do 401k catch-up contributions reduce taxable income?

The limits on elective deferrals and catch-up contributions are the same as for traditional 401(k)s. The difference is that contributions are made with post-tax dollars. That is, Roth contributions have already been taxed, and you cannot deduct these contributions from your taxable income for the year.

Can 401k be deducted from gross up calculation?

Your gross income is your total earnings received from all sources before taxes and other deductions. If your 401 (k) plan exempts your contributions from federal income tax withholding, then your contributions are not part of your gross income. Otherwise, your 401 (k) deductions are counted in your gross income.

Is FICA deduction before or after 401k deductions?

If you make 401(k) contributions, those will come from your gross pay before income taxes are deducted, but FICA taxes will be deducted before 401(k) deductions. Home Stocks Stocks +

How much should I contribute to a 401k?

Here’s how to determine the amount to save in your 401 (k) plan: The 401 (k) contribution limit is $19,500 in 2021. Workers age 50 and older can contribute an additional $6,500 in 2021. Qualifying for a 401 (k) match is the fastest way to build wealth for retirement. Many financial advisors recommend saving more than 10% of your income for retirement. Remember to increase your savings rate over time.

Is 401k considered a defined contribution plan?

A 401(a) is a defined contribution plan (employers contribute a set amount) generally offered to employees of the federal government, state governments, or Indian tribal governments, although private employers can establish them as well. Distributions are generally taxed.